We all know that most New Year’s Resolutions don’t make it past February let alone an entire year (actually, how many of your resolutions are really going strong after just a week?). What if sticking to that plan of just saving an extra 1% of your salary into your retirement account could have a lasting impact on the rest of your life? While that 1% seems like a small amount today, in 20 or 30 years, it can make a significant difference in your account balance at retirement.

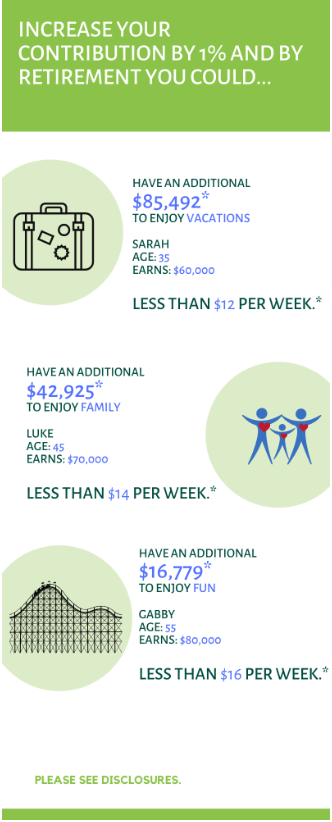

Consider these examples.

In these examples, small weekly amounts like $12, $14 and $16 can make a noticeable difference in your savings. The best part about 401(k) contributions is that they come right out of your paycheck so you probably won’t even miss those couple of dollars each week. If you don’t have a 401(k) through work, you can still save in a tax-advantaged account like an IRA or a Roth IRA.

This new year, challenge yourself to save a little more. Whether it’s a 1%, 3%, or even 5% increase, the extra savings today could make a significant impact in your retirement years. This could be a new year’s resolution worth following!

* Approximation based on a 1% increase in contribution rate. Continued employment from current age to retirement age, 67. We assume each example study (Sarah, Luke and Gabby) is exactly that age and will retire on their birthday at retirement age. Number of years of savings equals retirement age minus current age. Nominal investment growth rate is assumed to be 5.5%. Hypothetical nominal salary growth rate is assumed to be 4% (2.5% inflation + 1.5% real salary growth rate). All accumulated retirement savings amounts are shown in future (nominal) dollars. This assumes no loans or withdrawals are taken throughout the current age to retirement age. Your own plan account may earn more or less than this example and income taxes will be due when you withdraw from your account. Investing in this manner does not ensure a profit or guarantee against a loss in declining markets. Investing involves risk, including the risk of loss.